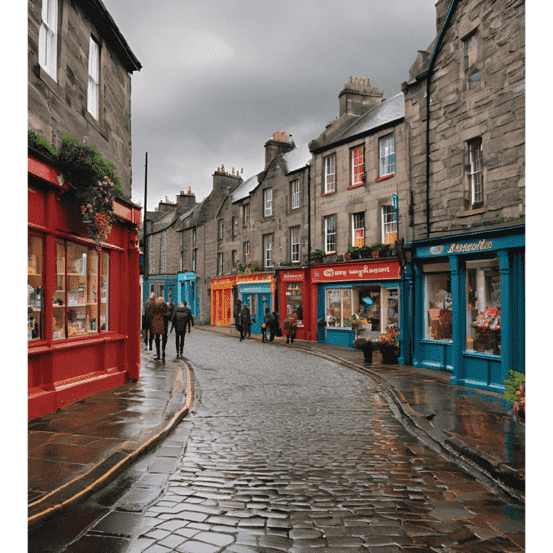

French Property Market: Recovery Signs Amidst Challenges

Discover six key insights from notaire data on the French property market's recovery post-Covid, despite ongoing low sales and prices.

French notaires have recently expressed an unexpectedly optimistic outlook regarding the French property market, as delineated in their latest report. Despite the prevailing challenges of low sales and declining prices, the rate of these declines appears to be decelerating, suggesting a potential inflection point in market trends that may persist into 2025.

The Notaires de France, an esteemed collective representing all notaires across the nation, diligently publishes a quarterly report that serves as the most comprehensive repository of information pertaining to the state of the French property market. This report amalgamates data from property transactions alongside insights into mortgage rates and the construction of new properties. However, it is worth noting that the compilation process necessitates a considerable amount of time, resulting in a reporting lag of approximately two quarters. The most recent complete data set extends to June 2024, although preliminary insights leading up to October 2024 are also available.

In examining the salient points illuminated by the data, we find cause for cautious optimism despite the ongoing sales slump. The figures reveal that a mere 780,000 properties were transacted between August 2023 and August 2024, marking a continued decline from previous years. This figure represents the nadir of the market slump that commenced in late 2021, when over 1.2 million properties exchanged hands during the 12-month period spanning August 2020 to 2021. Notably, the year-on-year decreases in sales for July and August 2024, when juxtaposed with 2023, fell below the 20% threshold—a statistic not observed since autumn 2023—indicating a potential resurgence in market activity.

The property market appears to be nearing the conclusion of its protracted downward cycle, which has persisted for two years. The European Central Bank's recent interest rate cuts, coupled with an expansion of zero-interest home loan offerings, are anticipated to bolster the number of mortgage offers, aligning with the broader market upturn. While confidence in the housing market remains subdued, it has exhibited a modest increase for three consecutive months as reported by the national statistics body, INSEE. This tempered optimism, albeit measured, is beginning to permeate the market landscape.

A cartographic analysis of house price fluctuations between spring 2023 and 2024 reveals that only three cities in mainland France experienced price increases during this period. In stark contrast to earlier reports indicating that numerous cities faced price declines exceeding 10% within a 12-month span, only Nantes in northwestern France has continued to witness such significant price reductions. For a comprehensive overview of price changes, including insights into the most and least expensive areas for property acquisition, one may refer to our accompanying article, which features a detailed map of average property values throughout France.

The variability in flat prices is noteworthy, with certain locales experiencing declines approaching 20%, while others have maintained relative price stability. Interestingly, tourist destinations have seen price increases throughout the downturn, as previously noted by notaires. However, the relentless price drops that have characterized the market for over a year appear to be abating. Between the first and second quarters of 2024, prices for all non-new-build properties (houses and flats) fell by a modest -0.5%. In contrast, the preceding quarter witnessed a more pronounced decline of -1.6%. Year-on-year comparisons for the second quarter of 2024 indicate an annual decrease of -5%, a slight improvement from the -5.2% recorded in the first quarter of 2024. Notaires predict that this figure could stabilize at around -2.6% year-on-year by November 2024, suggesting that prices may have begun to ascend during the summer months.

In the realm of Parisian real estate, an increasingly optimistic narrative is emerging. However, it is essential to acknowledge that price declines have been more pronounced in the capital and its surrounding regions. The Île-de-France region experienced year-on-year price drops of -7.2% in the second quarter of 2024, surpassing the national average decline of -5%. Furthermore, the quarterly comparison between the first and second quarters of 2024 revealed a decrease of -0.9% in the region, compared to the national figure of -0.5%. By November 2024, year-on-year price declines in the city and its inner suburbs for houses are projected to range between -4.5% and -4.3%, while flats are expected to see a more modest decline of -1.8%. This trend suggests a potential stabilization of prices in the city, with the price per square meter for flats now standing at €9,430—nearly double that of other regions in the country, yet approximately €1,000 per square meter less than pre-slump levels.

An intriguing demographic shift is also evident, as the proportion of elderly individuals selling their properties has markedly increased since the onset of 2024. Notably, 56% of overall sellers now comprise individuals aged 60 and above, reflecting a 4% increase since the beginning of the year. This trend is particularly pronounced among those aged 70 and older, who account for one-third of all sales, marking a 3% rise in this demographic. Conversely, individuals aged 50-59 represent 16% of sales, while those aged 40-49 account for 14%, and the 30-39 age group comprises 12%. Notably, individuals aged 30 and under constitute a mere 2% of overall sales. The average age of property sellers in France has now reached 61, a slight increase from 59 years and 10 months at the same point in 2023.

In the realm of mortgage lending, a discernible recovery trend is emerging. Following a market low of €6.9 billion in outstanding mortgage loans in March 2024, this figure has surged to €9.8 billion by August 2024. While July 2024 witnessed an even higher figure of €11.3 billion, the overall trend indicates an increase in loan offerings to replace maturing mortgages. As of the end of August 2024, interest rates have dipped to 3.59%, representing a decline of over 0.5% from their peak at the end of 2023 and a decrease from August 2023 levels. This marks the eighth consecutive month of falling mortgage rates, with further reductions anticipated through the end of the year.

Banks are mandated to adhere to specific criteria when extending mortgage offers, based on financial parameters such as income levels and property prices. Government regulations permit banks to deviate from these criteria in up to 20% of cases, primarily to assist first-time buyers. However, current practices indicate that banks are only exercising this flexibility in 15% of applications, a statistic that reflects their confidence in the market's stability, suggesting that they do not need to maximize their lending limits to maintain a robust flow of mortgage applications.

French Property Market: Recovery Signs Amidst Challenges

Greece: Europe’s Fourth Cheapest Real Estate Market

Greece: Europe’s Fourth Cheapest Real Estate Market

Explore why Greece stands out as one of Europe’s most economical real estate markets, attracting savvy investors seeking value and opportunity.

Surge in Scottish Home Sales: UK Real Estate Update

Surge in Scottish Home Sales: UK Real Estate Update

Scottish home sales and enquiries surged in October, with a third of surveyors reporting the fastest growth in years, signaling a vibrant market.

Spain: A Leading Market in European Real Estate

Spain: A Leading Market in European Real Estate

Explore how Spain is becoming one of Europe's most promising real estate markets, excelling in retail, logistics, and hotel sectors for strategic growth.

Greece Real Estate Market: Rise of Serviced Apartments

Greece Real Estate Market: Rise of Serviced Apartments

Explore the growing demand for serviced apartments in central Athens, where integrated hospitality services attract savvy investors in the Greece real estate market.

Home Prices Hit by Climate Change, J.P. Morgan Warns

Home Prices Hit by Climate Change, J.P. Morgan Warns

J.P. Morgan analysts reveal a negative link between climate risk and home price appreciation. Explore the emerging trends and their impact.